3 out of 25 FBR tax offices generate 60% of Income and Sales Tax Revenue: Are people in Lahore, Karachi and Islamabad more honest, or is there something else at play?

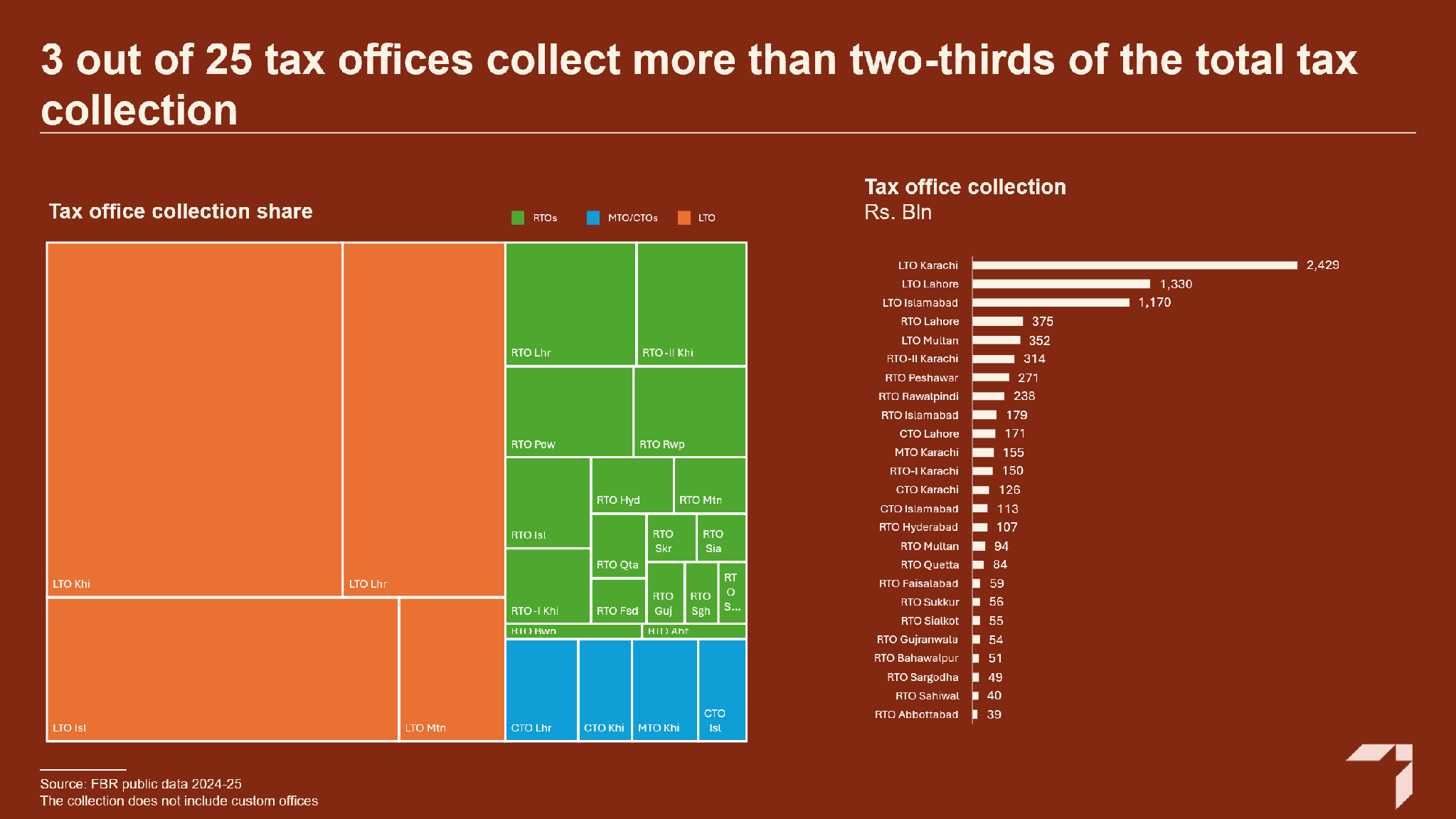

Three out of twenty-five field formations across the country accounted for approximately two-thirds of Pakistan’s total tax revenue in FY2024–25, according to publicly available data from the Federal Board of Revenue (FBR). These three Large Taxpayer Offices (LTOs), situated in Karachi, Lahore, and Islamabad, collected a staggering Rs. 5 trillion, almost 60% of FBR’s tax collection, excluding customs revenue. While a superficial glance might attribute this staggering concentration to the intense economic activity inherent to these urban hubs, or to a more compliant tax culture in the three large cities, a deeper dive into the composition of the taxpayers registered with these offices reveals a far more telling reality.

LTOs almost exclusively manage Pakistan’s largest corporate entities. Their portfolios include major commercial banks, prominent multinational corporations such as GSK, PepsiCo, and Philip Morris, and massive domestic conglomerates like Engro Fertilizers, OGDCL, and Bestway Cement. Consequently, the primary engine of Pakistan's tax collection relies on entities that are already deeply entrenched within the formal tax net. Because these companies are frequently listed on the stock exchange and maintain rigorously audited financial books, they present an easy target for compliance analysis, detailed audits, and the introduction of ad-hoc revenue-generating measures. In simple terms, they have no option but to be tax compliant.

A rough estimate of the revenue of these entities is between $60-$100 billion (Rs 17-30 trillion) per year. Now, think of the following. If the first $60-100 billion produces Rs 5 trillion in tax revenue, what does the rest of the $400 billion economy produce in tax returns?

Reviewing the remaining 22 FBR field formations reveals the reality. Average revenue per office drops off a steep precipice. The three corporate tax offices (CTOs), again in Karachi, Lahore, Islamabad, drop drastically to an average collection of just Rs141 billion per office, while the 17 regional tax offices (RTOs) bottom out at an average of Rs130 billion. The drastic dip in average collection in offices other than LTO in the same geography reinforces the earlier hypothesis.

This massive fiscal gap highlights a few realities. First, that beyond the large corporate entities working in the country, Pakistan’s economy is small, fragmented, and shy of entering a tax regime that it sees as both extortionate and bureaucratic, and also as giving them back nothing in return. Second, this correlates directly with the lack of documentation among small-and-medium enterprises (SMEs), a widespread absence of formal financial statements, and deeply entrenched, cash-based supply chains.

Unlocking revenue from this vast, quasi-informal segment requires consistent field intelligence and get your hands dirty approach to enforcement to drive compliance; capabilities that current field offices struggle to deploy effectively. It also implies creating an economic ecosystem where businesses and individuals see the benefits of entering Pakistan’s tax system, and where these businesses have the confidence that entering the tax net or honestly declaring returns will not induce them into a tax trap, where they become part of a small minority of compliant taxpayers in the country.

There is another conclusion also; that merely altering tax legislation or introducing advanced digital technologies will not inherently boost revenue collection across the board. Instead, without structural shifts in terms of how tax offices operate, and behavioral shifts in terms of how the state builds the credibility of the tax system with citizens, these interventions will only continue to squeeze the same narrow pool of corporate entities and individuals that already bear a disproportionate tax burden.

True reform demands a paradigm shift: moving the system from rate hikes to broadening the tax base; transitioning from a dependence on withholding taxes to actual income assessment; and shifting the focus from penalizing compliant corporate taxpayers to documenting non-compliant informal markets. To achieve this, the FBR’s field formations must be governed by a comprehensive operational framework. Rather than acting as mere collection agencies chasing soft targets, their primary mandates must pivot back to core tax operations, rigorous supply-chain monitoring, and targeted broadening of the tax base initiatives.