Pakistan’s Fiscal Challenge: No one wants to talk about spending!

Pakistan’s revenue challenges are well known. Its tax to GDP ratio is lower than peers and one of the lowest globally. There is a big grey economy outside of the tax net, with some estimates stating that the undocumented economy could be equal in size to the taxed economy. Agriculture, property, retail and trade continue to be undertaxed. Compliance is weak. Exemptions remain generous. It is true that Pakistan continues to need significant tax reform. But with all this, there is another elephant in the room that no one wants to talk about: Pakistan’s spending structure is unsustainable, and it outpaces any increases in revenue.

On the revenue side, at least there has been some progress. FBR receipts have risen from Rs 2.59 trillion in FY2014-15 to over Rs 11 trillion in FY2024-25. The tax-to-GDP ratio, while still exceptionally low, has finally improved to around 10.3 percent in FY2024-25. Repeated rate increases, the withdrawal of exemptions, tighter enforcement, super taxes, the increases in personal income tax rates, CVT on foreign assets – most of these measures continue to target already documented sectors and taxpayers, but at least all of this shows recognition of Pakistan’s need to increase revenue.

The numbers increasingly show that the crisis is not only about how much the state collects. It is about how much the state has structurally committed itself to spend. And yet, no one wants to talk about spending!

In the last decade, in nominal terms, total federal spending alone has increased by 4.4x, from Rs. 4.3 trillion in 2014-15 to Rs. 18.9 trillion in 2024-25. But more important than the nominal numbers, driven by devaluation and inflation, is the rigid structure of spending.

The single largest spending constraint Pakistan has is debt servicing, which has exploded. In 2014-15, debt servicing was around Rs. 781 billion, equivalent to less than 40% of FBR collection and had not yet touched a trillion rupees. By 2024-25, debt servicing, or interest payments, were budgeted at Rs 9.78 trillion, over 80% of FBR tax collection! Effectively, debt servicing absorbs the bulk of resources collected by FBR and necessitates further borrowing to finance basic Pakistan’s expenditure needs. Pakistan is caught in a debt trap that significantly limits the government’s ability to expand development spending, strengthen social protection, streamline service delivery or invest in productivity-enhancing infrastructure.

If anything, Pakistan’s expanding debt portfolio creates a perfect burning platform to reform other spending areas. But sadly, evidence points to no progress in this regard.

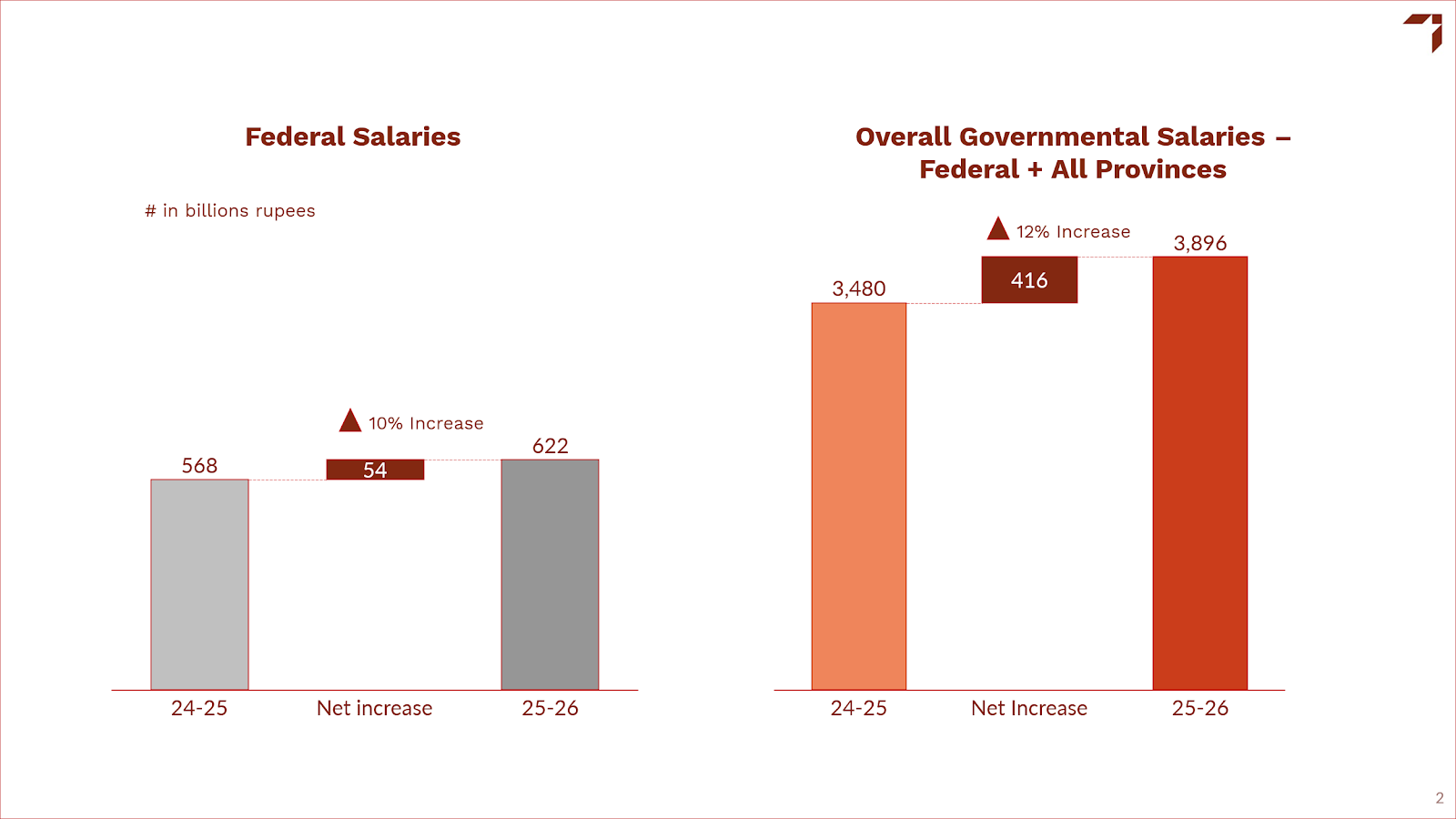

Specifically, take two large spending heads: salaries and pensions.

The salary and pension bill for the federal government in 2024-25 totaled Rs 1.55 trillion, Rs 283 billion or 18% greater than the previous year. However, this is only the tip of the iceberg, because pay and pensions increases in the federal government are tied to similar decisions in the provinces because of our unified pay structure.

Taking the federal government’s salary bill alone, excluding the military, basic pay was budgeted at Rs 538 billion in 2024-25. Similarly, the salary bills of all four provincial governments add up to approximately Rs 3.48 trillion for 2024-25. Following the announced pay increases and higher provincial allocations, the federal bill increased to Rs. 622 billion and the consolidated national salary bill for 2025-26 now stands at roughly Rs 3.9 trillion. This represents an increase of about Rs 416 billion in just one year, or around 12 percent (figure 1). This figure does not include hundreds of thousands of employees working in universities, autonomous bodies, and state-owned enterprises, which follow similar pay structures.

Figure 1

Similarly, while pensions in the federal government, including military pensions, amounted to Rs 1.014 trillion in the 2024-25 budget, when the national pension bill is added up by adding up the pension payments of the four provinces, total pension payments double to Rs 1.98 trillion. The increase in federal government pension spending, of Rs 213 billion, doubles to almost Rs 220 billion when increases across all four provinces are added. In 2025-26, the national pension bill increased to around Rs 2.2 trillion. Note that 20 years ago, the total pension spend nationally would have just been around Rs 20 billion, or 1% of annual national spend. Today, the spending on pensions is almost 10% of national spending!

Taken together, the combined burden of salaries and pensions illustrates the growing pressure on overall spending. In 2024-25, federal spending on basic pay and pensions alone amounted to roughly Rs 1.55 trillion, which increased to over Rs 1.63 trillion in 2025-26. When provincial governments are included, the combined national bill for salaries and pensions increased from roughly Rs 5.46 trillion in 2024-25 to about Rs 6.1 trillion in 2025-26. In other words, more than Rs 6 trillion in public resources are now committed annually to wages and retirement benefits across all tiers of government.

Now place that next to debt servicing of Rs 9.78 trillion. Together, debt servicing, pay and pensions and the basic machinery of government absorb more annually than debt servicing, and the pay and pension of government employees. In effect, most of the fiscal envelope is structurally pre-committed. This explains why incremental revenue gains do not translate into policy flexibility. Higher tax collection is largely absorbed by debt servicing, salaries, pensions, and other fixed obligations. Development spending becomes residual rather than strategic. The result is a fiscal structure under constant pressure. Pakistan returns repeatedly to stabilization programs not only because it collects too little, but because its recurring commitments expand faster than sustainable revenue.

There is no way to fix the fiscal deficit without fixing pay and pensions. Can Pakistan afford hundreds of thousands of permanent public sector jobs that are unproductive, and bloat the public sector, but are only a drop in the ocean in terms of job creation in the overall labour force? Can Pakistan afford a pay and employment structure in the public sector that doesn’t award excellence, or differentiate between good and bad performers? Can Pakistan afford a Rs 2.5 trillion annual pension bill, growing at over 20% annually, that is, uniquely for anywhere in the world, unfunded? Or should Pakistan continue to add over Rs 1 trillion and increasing every year to its national pay and pension bill, ensuring that any fiscal space created through tax reform cannot be put to any productive use?

Pakistan unquestionably needs stronger taxation, a broader base, and better compliance. But fiscal sustainability requires equal emphasis on expenditure reform. Debt dynamics must be managed more prudently. Pension systems require restructuring. Civil administration must become leaner and more efficient. Federal and provincial spending priorities must align more closely with productivity and growth.

Without such reforms, additional revenue will continue to finance survival rather than stability. The fiscal debate must therefore move beyond revenue alone. The real question is not simply how much the state collects. It is how much the state has structurally locked itself into spending.